Trading offers a wide world of opportunities to traders new and experienced alike.

It’s unfortunate, but trading profitably with any level of consistency often takes time and effort for a trader to develop their approach. Along the way are many hurdles and perhaps even more unfortunately, quite a few of those hurdles can be self-imposed.

It’s not abnormal for a trader to become ‘their own worst enemy.’ And once a trader has begun that downward spiral of self-doubt coupled with eroding confidence, winning trades may seem like they can allude for eternity.

This is trading stress, and it’s an inevitable part of the game. But for traders to find the long-term success we spoke of above, precautions must be made to ensure that this trap of self-doubt does not snare another victim.

What follows are three of the most prominent ways that traders can reduce trading stress, allowing them to focus on what matters most.

Trust the Trading Plan

Do you have a trading plan? If not, you certainly should. This is advice that is similar to: ‘Eat your vegetables,’ or ‘get 8 hours of sleep per night,’ that we all know we should follow in interests of our long-term success, but for whatever reason we might find it difficult to actually do.

Regardless of your background or experience level, you should have a trading plan. This functions like a trader’s ‘Constitution’ that defines how, why, and where you will be operating.

You can write down your rules in your trading plan, such as “I will not allow one ‘idea (or trade)’ to take away more than 2% of my trading capital.”

This way, when you violate your own rules – you know for a fact that you did something that you hadn’t planned or wanted to do. You’ve violated your own constitution, and you know it.

Once you have a well written trading plan, you can simply follow and trust that the plan will work.

Keep the Bigger Picture in Mind

I know that this sounds overly-simplistic, but this defines the conundrum that many new traders face. You cannot tell the future, yet – as a trader – your job is to risk your own money on future price movements that may or may not happen.

As human beings, we often equate success with ‘being right.’ And when trading, we often suffer from a degree of myopia, in which we want to try to see each and every trade to profitability.

This often means that when we have a losing trade, we hold on in the hope that prices move back in our direction so that we can close this out as a winner. We’re often displaying greed in these scenarios, when in fact we should be displaying fear.

Or, if we get a small gain in a trade, we often close it out quickly for the fear of price moving against us – becoming a loss. This is when we should be displaying greed, not fear; and default human nature often gives us the exact opposite of what we need.

But if you take a step back, you’ll probably realize that any one trade isn’t going to make your career, or have a large impact on your quality of life; at least it shouldn’t, and if it does, you are risking far too much on just one idea or hypothesis. Any one trade should be but one of a thousand insignificant trades that you place in your career.

If you have a particularly bad day, don’t shy away from taking the rest of the afternoon off, or going for a run, or whatever you have to do to take a step back. Markets will be here tomorrow, and there is no such thing as an opportunity that is too good to pass up when trading.

Remember – Trading opportunities are infinite, trading capital is not.

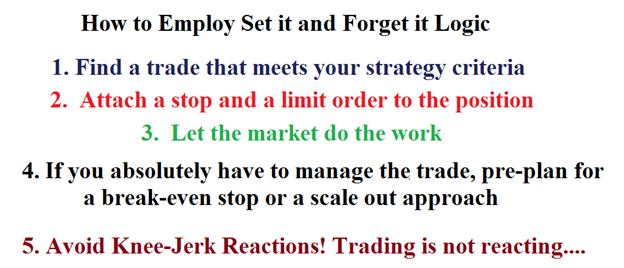

Employ ‘Set it and Forget it’ Logic

One of the big reasons that traders gravitate towards markets is that the potential to make money with a small amount of time is extremely attractive. In most jobs, one is paid a wage for a set amount of hours worked, and that’s all that there is. In trading, you can define your own income, and you can work considerably less than everyone else in something that can be so fun to do.

But, along the journey of learning to trade, the point of working less often becomes obscured by the fact that trading is not easy. Many traders often pick up the idea that they need to manage each and every trade as if it were a surgical operation.

As long as the first two principals are followed, this is absolutely not the case, and this sense of micro-management may even be doing you a disfavor. Just like we mentioned previously, traders often gain a sense of myopia when managing positions. This could allow traders to hold on to losers for far too long, or to cut winners far too short.

Just like you can’t predict the future at the outset of a trade, you can’t predict the future after the trade has been opened. Surely, market conditions, prices, fundamental factors all change – but regardless of this fact you will still not be able to predict what will happen next, so you shouldn’t manage your trade as if you can.

By employing ‘Set it and Forget it’ logic to one’s positions, they can open the trade with a stop and a limit set – and then let the trade work. If the trader’s strategy is strong enough, over the long-term, this type of logic should present numerous benefits. If you absolutely HAVE to modify your trade, perhaps allow in the trading plan for a Break-even stop at a pre-determined time, or the ability to scale out of the position as the trade moves in your favor; but nothing so brash as manually closing a position with a 50 point gain when you had initially sought 200 point, simply because of the fear of allowing that 50 point gain to become a loser. Or conversely, if you opened a position with a 100 point stop and the trade is sitting at a loss of 90 point, don’t remove the stop simply because you hope that prices will come back, bargaining with yourself that ‘if this trade comes back to break-even, ill close it and never do this again.’

Because over the long run, looking at the bigger picture, that trade probably will not come back, and removing your stops simply for the greedy hope that it might could cost you a significant amount of money.

Useful tips 🙂